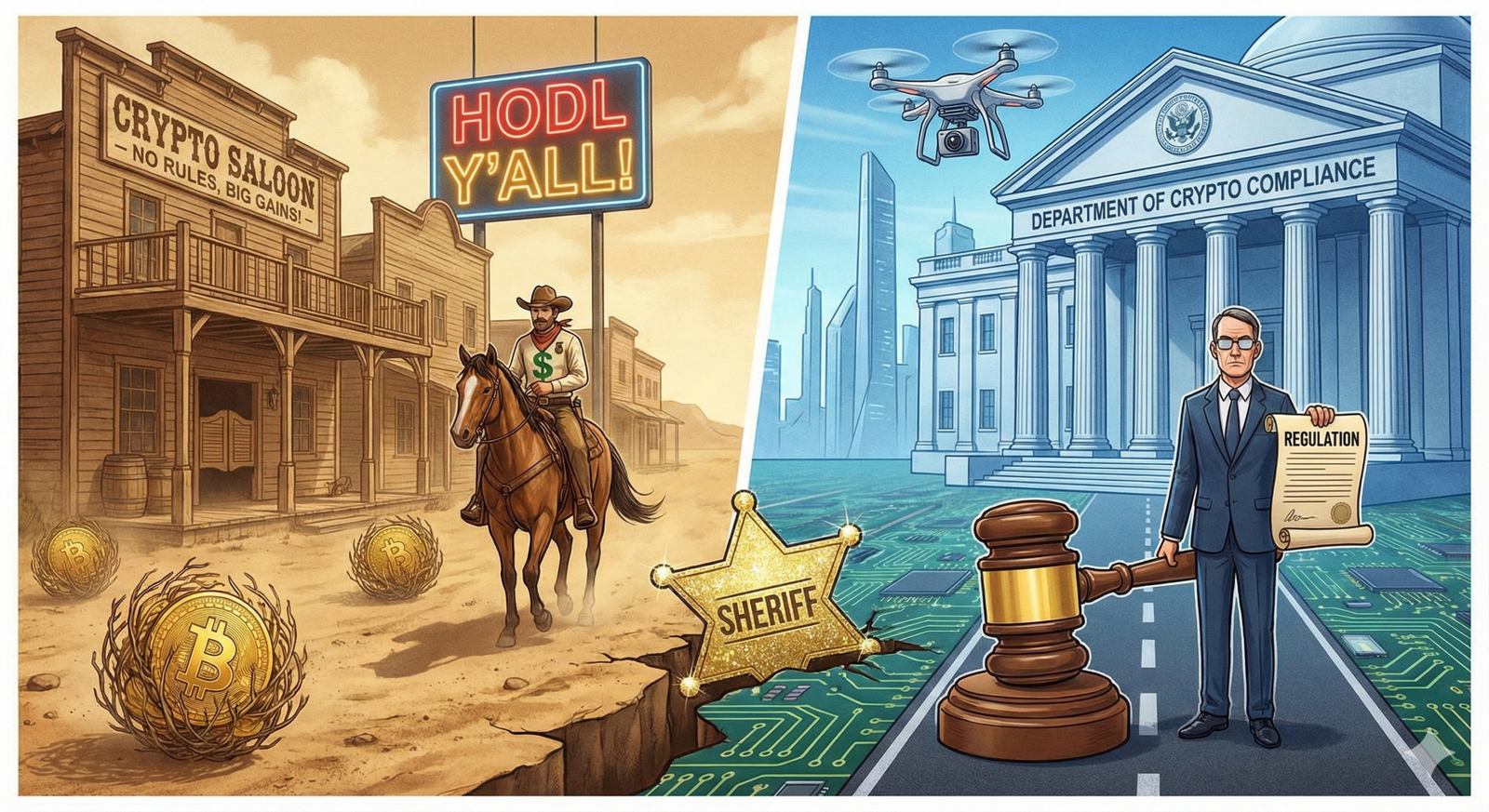

For over a decade, the crypto currency market in the United States has operated much like the American frontier of the 19th century: vast, promising, occasionally lawless, and defined by tremendous booms and devastating busts. Fortunes were made overnight in a deregulated environment, while catastrophic failures like the collapse of FTX wiped out billions in consumer funds in days.

This era of the “Wild West” is rapidly drawing to a close.

As digital assets mature from niche curiosities into significant financial instruments held by millions of Americans and major institutions, Washington D.C. is stepping in. The debate is no longer if crypto should be regulated, but how. For everyday investors trying to navigate this volatile market, understanding the shifting sands of federal policy is now as crucial as understanding blockchain technology itself.

Here is an examination of the current regulatory landscape, potential legislative actions on the horizon, and what the inevitable arrival of the “sheriff” means for your portfolio.

The Current Landscape: Regulation by Enforcement

To understand where US crypto regulation is going, we must first understand the confusing state of where it is right now. Currently, there is no single comprehensive framework governing digital assets in the US. Instead, the market is navigating a patchwork of mostly outdated financial laws applied by warring agencies.

The Turf War: SEC vs. CFTC

The central conflict in US crypto policy is a jurisdictional tug-of-war between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

The core question is simple, yet unresolved: Are cryptocurrencies securities (like stocks) or commodities (like gold or wheat)?

Under Chair Gary Gensler, the SEC has taken an aggressive stance, arguing that the vast majority of cryptocurrencies—excluding Bitcoin—meet the definition of a security. If an asset is a security, the issuer and the exchanges trading it must register with the SEC and adhere to strict investor protection and disclosure rules.

Conversely, many in the industry argue that crypto assets behave more like commodities, which would fall under the purview of the CFTC. The CFTC is generally viewed by the industry as a more favorable, though still rigorous, regulator.

The “Regulation by Enforcement” Era

Because Congress has not yet passed laws specifically defining digital assets, agencies—primarily the SEC—have resorted to “regulation by enforcement.” Rather than issuing clear proactive rules, they sue major industry players for violating existing securities laws. High-profile lawsuits against major exchanges like Coinbase and Binance are prime examples of this strategy.

While this approach punishes bad actors, critics argue it creates a hostile environment for innovation, forcing legitimate US crypto businesses to operate in a fog of legal uncertainty or move offshore.

The Watershed Moment: Spot Bitcoin ETFs

Despite the aggressive enforcement posture, 2024 marked a massive turning point for crypto legitimacy. After years of denials, the SEC reluctantly approved Spot Bitcoin Exchange-Traded Funds (ETFs).

This was a watershed moment. It allowed everyday investors to gain exposure to Bitcoin prices through traditional brokerage accounts like Fidelity or Schwab, without needing to manage digital wallets or private keys. The approval signaled a forced acknowledgment from federal regulators that crypto is a permanent fixture in the financial landscape, bridging the gap between traditional finance (TradFi) and decentralized finance (DeFi).

On the Horizon: Key Legislative Areas to Watch

Regulation by enforcement is unsustainable long-term. Both regulators and industry leaders are clamoring for Congress to provide clarity. While political gridlock often slows progress, several key areas of legislation are taking shape.

1. Taming Stablecoins in crypto

The most likely piece of crypto legislation to pass in the near future involves stablecoins—cryptocurrencies pegged to a fiat currency like the US Dollar (e.g., USDC or USDT).

Regulators, particularly at the Treasury Department and the Federal Reserve, view unregulated stablecoins as a potential threat to financial stability. If a major stablecoin issuer failed to back their tokens 1:1 with real dollars during a “bank run,” it could trigger wider financial panic. Future legislation will almost certainly mandate strict reserve requirements, regular audits, and federal supervision for stablecoin issuers, treating them similarly to narrow banks.

2. Defining the Asset Class in crypto

Congress is under pressure to finally settle the “security vs. commodity” debate. Bipartisan bills have been proposed that attempt to create a litmus test for digital assets.

The general legislative trend suggests a hybrid model: Bitcoin and perhaps Ethereum would be definitively classified as commodities regulated by the CFTC, while many newer, smaller tokens sold to raise capital for centralized projects would remain under SEC jurisdiction.

3. Exchange and Custody Rules in crypto

Post-FTX, protecting consumer deposits is paramount. Future laws will likely forbid exchanges from commingling customer funds with their own corporate operational funds. We can also expect stricter mandates regarding cybersecurity standards and mandatory disclosures about the risks of trading.

What These Changes Mean for Everyday Investors

The transition from a Wild West to a regulated market will profoundly change the user experience for retail investors. It comes with significant trade-offs.

The Pros: Legitimacy and Safety

- Reduced Fraud Risk: Stricter oversight of exchanges and token issuers should significantly reduce the number of “rug pulls,” Ponzi schemes, and exchange collapses that have plagued the industry.

- Institutional Adoption: Clear rules provide the green light for massive institutional investors (pension funds, endowments) to enter the space safely. This influx of capital could stabilize markets and potentially drive long-term value appreciation for established assets like Bitcoin.

- Easier Access: As seen with ETFs, regulation bridges the gap with traditional finance, making it easier to invest in crypto through familiar platforms.

The Cons: Friction and Surveillance

- The End of Anonymity: The days of anonymous trading are numbered. Expect much stricter Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements across all US-accessible platforms. The IRS will also gain clearer view into crypto transactions for tax purposes.

- Higher Barriers to Entry for New Projects: If new tokens are classified as securities, the cost and legal burden of launching a new crypto project in the US will skyrocket. This could stifle smaller-scale innovation or push it entirely overseas.

- Possible Profit Squeeze: A mature, regulated market is often less volatile. While this means fewer 80% crashes, it might also mean fewer opportunities for the 100x overnight gains that attracted many to the “Wild West” in the first place.

Conclusion: The End of the Frontier

The US cryptocurrency market is in the midst of necessary, uncomfortable growing pains. The “move fast and break things” ethos that defined the last decade is colliding with the rigid reality of federal financial law.

For the everyday investor, the future of crypto in the US will be characterized by a trade-off between raw opportunity and regulated stability. The frontier is closing. While some of the unchecked freedom of the early days will be lost, what replaces it will likely be a more robust, trustworthy, and integrated financial system. The Wild West is becoming civilized, and for the long-term viability of the asset class, that is ultimately a good thing.