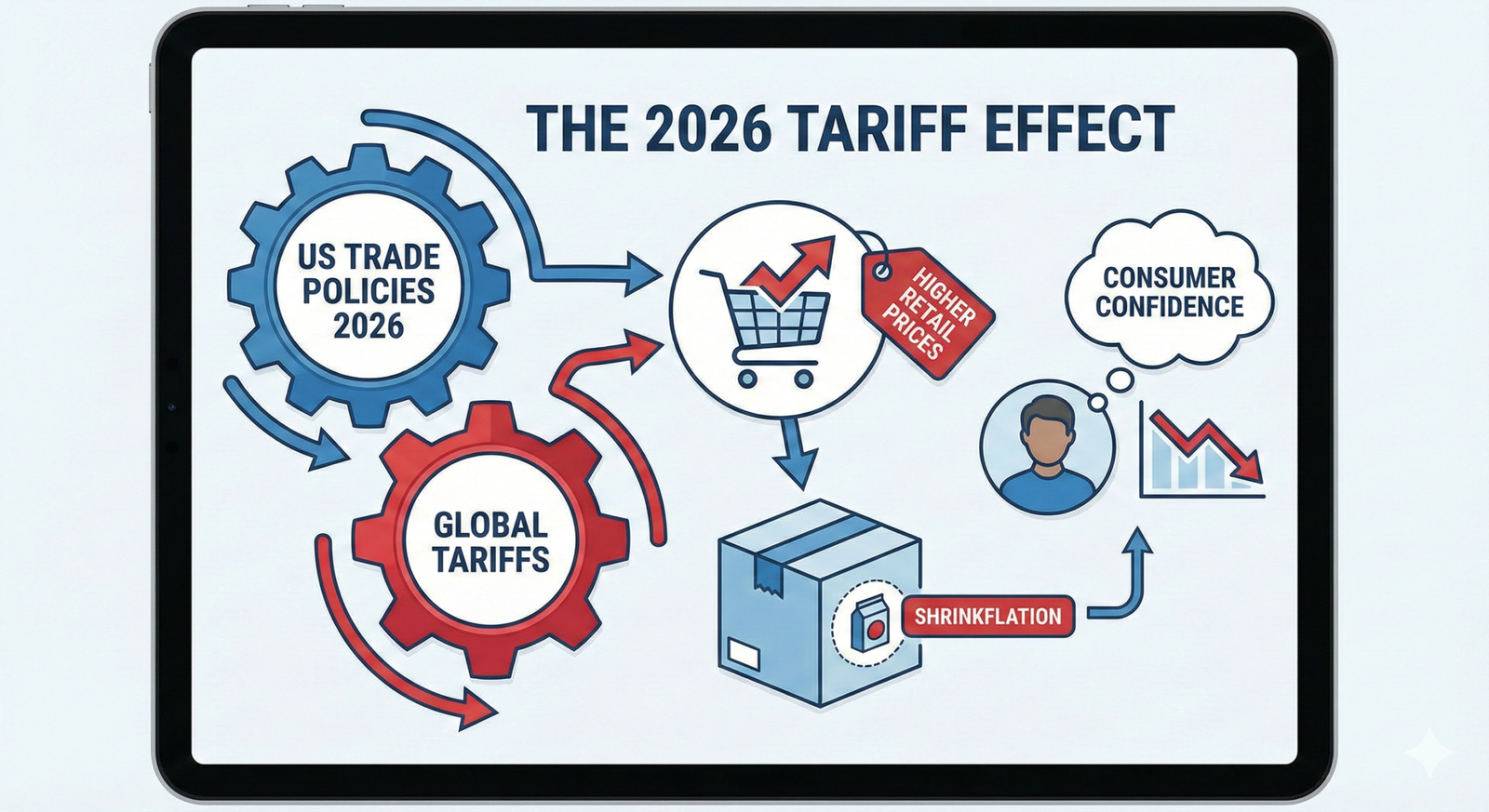

The United States economic landscape in 2026 has been defined by a singular, overwhelming force: trade policy whiplash. Within a historic 24-hour window in February 2026, the bedrock of recent US trade policy was upended. Only to be immediately replaced by a new, sweeping framework of import surcharges. For retailers and consumers, this “tariff tug-of-war” is no longer just a macroeconomic talking point—it is a daily reality fundamentally altering retail prices. Supply chain logistics, and consumer confidence.

So, as businesses navigate the highest effective tariff rates seen in generations. The critical question remains: who is ultimately footing the bill? In this article, we explore the chaotic 2026 US trade policy landscape. Analyze how new global tariffs are transmitting into retail prices, and unpack the resulting impact on consumer behavior.

The 2026 Trade Landscape: A Year of Unprecedented Volatility

To understand the current retail environment, one must look at the legal and political whirlwind that defined early 2026. Prior to February, the US operated under a broad umbrella of tariffs enacted via the International Emergency Economic Powers Act (IEEPA). Which pushed the average effective tariff rate to roughly 16%—the highest level since 1936.

However, on February 20, 2026, the US Supreme Court issued a landmark 6-3 decision striking down the president’s authority to use IEEPA to impose tariffs. For a brief moment, the effective tariff rate plummeted. But the reprieve was fleeting. Within hours, the White House pivoted, invoking Section 122 of the Trade Act to implement a temporary 150-day global import surcharge, initially set at 10% and quickly increased to 15%.+2

This rapid shift created massive uncertainty. While Section 122 provides exemptions for critical minerals, certain pharmaceuticals, and select agricultural goods, it casts a wide net over consumer goods. Today, the effective US tariff rate hovers around 13.7%. For the retail sector, this legal whiplash means that supply chain forecasting has shifted from a quarterly exercise to a daily scramble, with profound implications for the cost of goods sold (COGS).+1

The Pass-Through Effect: How Tariffs Reach the Retail Shelf in Trade

When global tariffs are enacted, they are technically paid by the importing US companies, not foreign governments. The debate among economists has long centered on how much of that cost is absorbed by corporate margins versus passed through to the consumer. In 2026, the data paints a clear, albeit complex, picture of retail price inflation.

The Rise of “Shrinkflation” in Retail

Also, recent economic analyses utilizing retail scanner and barcode data reveal a fascinating trend in how tariffs are masked. While direct “pass-through” into the baseline retail price of a good is estimated at around 14%, the pass-through into the price per unit weight is significantly higher, at nearly 44%.

Instead of slapping a drastically higher price tag on a product. Which immediately damages consumer confidence—retailers and manufacturers are leaning heavily into product turnover and “shrinkflation.” Consumers are paying slightly more, but they are receiving notably smaller package sizes.

Sector-Specific Price Shocks

The impact of shifting US trade policies is not felt equally across all retail categories:

- Beauty, Cosmetics, and Apparel: These sectors, highly reliant on foreign manufacturing and raw materials, have seen marked price adjustments. So, data from early 2026 shows that an overwhelming majority of global fashion brands plan to pass tariff-related costs directly to consumers. Leading to noticeable drops in revenue and average order value (AOV) in these categories.

- Electronics and Appliances: While some tech components were granted exemptions under the new Section 122 rules. Historical legacy tariffs under Section 301 continue to keep prices artificially high for consumer electronics and household furnishings.

- Domestic Substitutes: Interestingly, as imported goods rise in price. Domestic producers often raise their prices in tandem, a phenomenon known as competitive pricing. This means even goods manufactured entirely within the US are seeing tariff-induced inflation.

The Hit to Consumer Confidence and Purchasing Power

The ultimate casualty of the 2026 tariff tug-of-war is the American consumer. As inflation stubbornly hovers closer to 3% rather than the Federal Reserve’s 2% target, the compounding effect of tariffs is creating a “stagflation lite” scenario—a combination of rising prices and a cooling job market.

The Household Financial Burden

Economic models from institutions like the Tax Foundation and the Yale Budget Lab estimate that the current tariff regime will result in a loss of purchasing power for the average US household ranging from $600 to over $1,300 in 2026 alone.

This acts as a regressive, invisible tax. Disproportionately affecting low- and middle-income households who spend a larger share of their income on heavily tariffed consumer goods.

The Value-Seeking Consumer

With purchasing power eroding, consumer confidence is taking a measurable hit. The post-pandemic spending spree—characterized by high discretionary spending and revenge travel—has definitively ended. In 2026, the retail market will be defined by the “value-seeking consumer.”

- Fewer Items Per Basket: Retailers are reporting steady declines in the number of items purchased per transaction.

- Prioritizing Essentials: Discretionary spending is crowded out as a higher percentage of the household budget goes toward basic groceries and essential goods.

- Brand Loyalty Erosion: Consumers are increasingly abandoning brand loyalty in favor of white-label or store-brand products that offer better cost-to-weight ratios.

Supply Chain Scrambles and the Inventory Chess Game

Behind the scenes, the volatility of US trade policies is forcing retailers into an aggressive game of inventory chess. The temporary nature of the 15% Section 122 tariffs—which are scheduled to expire in July 2026 unless extended or replaced by Congress or other statutory authorities—has created bizarre market incentives.

To navigate this, large-scale importers are aggressively utilizing customs-bonded warehouses and Foreign Trade Zones (FTZs). By staging inventory in these zones, retailers can legally delay the entry of goods into US commerce. They are essentially waiting for potential “gap periods” in tariff enforcement. Hoping to release goods into the market when the effective tariff rate temporarily dips.

However, this strategy requires massive capital reserves and sophisticated logistics, advantages that small and medium-sized enterprises (SMEs) simply do not have. Consequently, the 2026 tariff environment is inherently tilting the playing field toward massive multinational retailers who can afford to play the long game.

Conclusion to Trade

The 2026 trade landscape is a testament to the profound ripple effects of protectionist economic policy. The tug-of-war between the judicial branch and the executive branch over tariff authority has resulted in unprecedented volatility. For the retail sector, the reality is stark: supply chain costs have skyrocketed, and the tools used to mitigate them—from shrinkflation to warehouse staging—are being stretched to their limits.

Ultimately, shifting US trade policies and new global tariffs are successfully doing what they are mathematically designed to do: raising the cost of imported goods. But as retail prices climb and household purchasing power drops by upwards of $1,000 this year. Consumer confidence is bearing the brunt of the impact. Until a stable, predictable, and long-term trade framework is established. Retailers and consumers alike will remain caught in the middle of the tug-of-war.